A Parent’s Guide to Teaching Kids About Finances – Aug. ‘26

When is the best time to start talking to your kids about money? As soon as possible. The sooner you instill healthy financial habits, the better. According to a 2017 T. Rowe Price survey, 69% of parents have some form of reluctance when it comes to talking about money with their kids. It’s never too late to start having conversations around money with your kids or to dive a little deeper into personal finances. Here are some age-appropriate ways you can help your children plan for their financial future:

Preschoolers and kindergartners

- Use a clear jar for savings – Using a clear jar to collect savings helps kids visualize their money, rather than a opaque piggy bank. It teaches the lesson that when you save money, it actually grows.

- Let them participate – Teach them the reality that items cost money by letting them physically hand cash to a cashier at a restaurant or store. They need more than just being told about how money works, they need ways to put concepts into action.

- Lead by example –Just like any other value parents want to instill in their kids, actions teach more effectively than words. Children begin learning about saving and spending between ages 3-5. Set a healthy example around money – your kids are likely to carry this view around finances into adulthood.

Elementary and middle schoolers

- Give commissions – Instead of a weekly allowance, pay kids for completing household chores. Taking out the trash, mowing the lawn, and cleaning their room are ways to show that money isn’t given but earned.

- Teach money values – You don’t need to disclose your salary or bank statements to your kids to teach them the basics of saving, budgeting, spending and giving. Consistently instilling values and teaching them the power of delayed gratification, following a simple budget, spending money wisely, and practicing generosity will stick with them throughout their lives.

- Practice contentment – Elementary and middle school is the age where kids may start to be influenced by advertisements and social media or start comparing their clothes or possessions to their classmates’. Avoid impulsive purchases and consider a low- or no-spend summer to encourage them to appreciate what they already have.

Teenagers

- Set up a simple bank account – By the time kids are teenagers, it’s time to set them up with a simple bank account, like Student Checking with WSB. Giving them this responsibility, no matter how little income they have, prepares them for the future when they have additional responsibilities and money.

- Introduce them to investing – We all wish we knew about compound growth earlier on, which is exactly why introducing investing to your teens at an early age is incredibly impactful. There are investment accounts specifically for teenagers and getting them started early will have them ahead of the game by the time they enter the professional world.

- Help them figure out ways to make money – Help your teen find jobs they can work over summer, spring, and fall breaks. Better yet, if they have a hobby or skill they can turn into a side hustle, help them turn their passion into a profit and encourage entrepreneurship.

The Newest Wave of Amazon Scam Texts and Phone Calls – July ‘26

One way to spot a scam is to understand its mechanics. A new and complicated scam starts with a call or text message about a suspicious charge on your Amazon account. Or maybe this time, they’re sending texts claiming there’s a problem with something you bought. They offer a refund if you click a link — but instead, it’s a phishing scam to steal your money or personal information or a scammer with an elaborate story about fraud using your identity that ends with you draining your bank or retirement accounts.

Here’s what to know about these scam scenarios.

It’s not Amazon calling. Scammers spoof their phone number to make it look like it’s Amazon calling. Don’t trust the number in your caller ID and don’t trust what the caller tells you. Worried about a suspicious purchase on Amazon? Log in through the website or app. Don’t call back the number that called you or a number someone left in a voicemail or text message.

Don’t click links in unexpected texts — and don’t respond to them. If you think the message could be legit, contact the company using a phone number, email, or website you know is real — not the info from the text.

No one legitimate will tell you to keep it a secret. If there’s a problem with your account or identity, always talk about it with someone you trust — especially if the stranger on the phone says it’s serious or involves a crime or claims to be from the government. That’s a scam.

No one used your Social Security number to open fraudulent accounts in your name. Scammers say this to scare you — don’t trust the person on the phone. To know for sure, get an instant copy of your credit report online for free and look for accounts you don’t recognize. Visit (or have someone help you visit) AnnualCreditReport.com.

Don’t believe a caller who says you’ll be immediately arrested for account fraud. That’s a scam. If someone stole your identity to open fraudulent accounts, complete an FTC identity theft report at IdentityTheft.gov, then put an extended fraud alert on your credit report. Do not transfer money or drain your savings to protect it from fraud.

Check your Amazon account. If you’re worried, log in through the Amazon website or app — don’t use the link in the text — to see if there’s a problem with or recall on anything you’ve ordered.

{kind=link}

- Send unwanted texts to 7726 (SPAM) or use your phone’s “report junk” option. Once you’ve reported it, delete the message.

Learn more about how to get fewer spam texts. And if you spot a scam, tell the FTC at ReportFraud.ftc.gov.

This article is a combination of two articles from the FTC. Click the links below for more information:

https://consumer.ftc.gov/consumer-alerts/2025/07/scammy-texts-offering-refunds-amazon-purchases

Five Money Habits to Help Build Financial Independence – July ‘26

July 1st is National Financial Freedom Day, a reminder that financial independence is something worth pursuing, not just hoping for. It’s the point where your savings, investments and income give you real choices. Most people want it but far fewer achieve it. The underlying reason is often not income, but financial habits.

Washington State Bank is highlighting five practical money habits that can help move financial independence closer and make long-term goals feel more achievable. Here are five common habits that can help make financial independence more attainable:

- Start saving and investing

Time is the most powerful force in personal finance. According to the Federal Reserve, roughly one-quarter of U.S. adults have no retirement savings, while Yahoo Finance reports among those ages 55–64, the average retirement balance is about $271,320 and the median is $95,642. Waiting even five years to start can cost tens of thousands in long-term growth. Starting small always beats starting late.

- Pay down high-interest debt

High-interest debt destroys wealth because while debt grows, the ability to save does not. According to the Federal Reserve Bank of New York, Americans collectively owe more than $1.25 trillion in credit card debt. The average household carries around $9,300 in credit card debt at an average annual percentage rate of approximately 22%, according to data from The Motley Fool. At that rate, a $5,000 balance paid with minimum payments can take more than a decade to eliminate.

- Build an emergency fund

Without an emergency fund, any unexpected expense can trigger a financial setback that takes years to recover from. According to Bankrate, 27% of U.S. adults have no emergency savings whatsoever. Financial experts recommend building a fund covering three to six months of essential expenses before aggressively pursuing other financial goals.

- Mindful spending

Today’s spending environment is designed to pull money out of pockets, and it works. According to Capital One, the average American spent roughly $282 per month, or more than $3,300 annually, on impulse purchases in just one year. Over a decade, that is more than $33,000 that could have gone toward savings or debt payoff. A 24-hour waiting period before nonessential purchases is a simple and effective habit reset.

- Create a budget

A budget is simply a plan for your money. Without one, spending happens reactively. According to a recent LendingClub study, approximately 53% of Americans are living paycheck to paycheck, including more than 20% of households earning $150,000 or more. Income alone does not guarantee financial security. A plan does.

Take the Next Step

Our staff can help you save for the future with everything from a simple Savings Account to an IRA to meet your goals in life. Stop into your nearest WSB branch today or give us a call at

(800) 714-2287 to get started.

Protecting Older Americans Against Financial Exploitation - Jun. '26

In recognition of World Elder Abuse Awareness Day (WEAAD), Washington State Bank is joining The Independent Community Bankers of America® (ICBA) to raise awareness of elder financial abuse and share resources that help protect older Americans from exploitation.

According to the Financial Crimes Enforcement Network (FinCEN), financial institutions reported more than $27 billion in suspected elder financial exploitation over a recent one-year period. However, the true scale of elder financial exploitation may be even higher with only 1 in 44 cases of financial abuse reported.

Washington State Bank and ICBA offer the following tips to help prevent elder financial abuse:

- Safeguard financial documents. Secure checkbooks, account information, bank statements, and legal documents in a locked, secure location or safe deposit box.

- Monitor accounts regularly. Review financial statements and credit reports frequently for signs of unauthorized or unusual transactions

- Be cautious with personal information. Never share bank account numbers, PINs, or Social Security numbers with unsolicited callers, emails, or texts.

- Establish trusted financial caregivers. Work with your banker and attorney to assign a power of attorney or other trusted contacts to assist with financial management, if necessary.

- Leverage your community banker’s expertise for fraud education, financial planning assistance, and resources to help identify and avoid scams.

- Report suspected abuse immediately. Contact your bank, adult protective services, or law enforcement if you suspect financial exploitation

World Elder Abuse Awareness Day, observed annually on June 15, was established by the International Network for the Prevention of Elder Abuse and recognized by the United Nations to raise global awareness and encourage action to combat elder abuse. To learn more about elder financial abuse and prevention strategies, visit icba.org/eldercare.

About ICBA

The Independent Community Bankers of America® has one mission: to create and promote an environment where community banks flourish. We power the potential of the nation’s community banks through effective advocacy, education, and innovation.

As local and trusted sources of credit, America’s community banks leverage their relationship-based business model and innovative offerings to channel deposits into the neighborhoods they serve, creating jobs, fostering economic prosperity, and fueling their customers’ financial goals and dreams. For more information, visit ICBA’s website at icba.org.

Laying the Groundwork for Your First Home – June ‘26

June is American Housing Month, a great reminder that preparation and knowledge can help first-time homebuyers feel confident when entering the housing market. According to the National Association of Realtors (NAR), homeownership continues to be one of the primary ways Americans build long-term financial stability.

Homeownership also remains a meaningful financial milestone. The NAR states that delaying homeownership can impact long-term wealth building. If you are considering buying a home, here are several important factors to review before starting your home search.

How much have you saved?

Start with a clear picture of your savings. Down payments typically range from 5% to 20% of the purchase price, depending on the loan program. In addition to your down payment, you will need funds for closing costs and moving expenses.

It is also important to maintain an emergency fund. Financial experts recommend keeping three to six months of living expenses in reserve to cover unexpected costs.

How much debt are you carrying?

Review your current financial obligations, including car loans, credit cards and student loans. Lenders evaluate your debt-to-income ratio when determining loan eligibility. In general, total debt payments should remain manageable relative to your income. Resist making last-minute purchases that could impact loan eligibility.

As a general guideline, housing costs – including mortgage, property taxes and insurance – are often recommended to stay within 25% to 30% of gross monthly income.

What is your credit profile?

Your credit score plays a significant role in qualifying for a mortgage and securing a competitive interest rate. A stronger credit history can lead to better loan terms and lower monthly payments.

If your credit score needs improvement, take time before applying to reduce outstanding balances and make consistent, on-time payments that can help strengthen your position.

Have you planned for the full cost of homeownership?

Beyond the mortgage payment, homeownership includes additional expenses such as utilities, maintenance, property taxes and homeowners insurance. Buyers should also consider potential repairs and routine upkeep. According to a study by Bankrate, the average homeowner in Iowa spent about $15,737 annually on costs beyond their mortgage payment in 2025, including property taxes, insurance, utilities and routine maintenance, painting a picture of the importance of planning for the full cost of homeownership.

Creating a realistic monthly budget can help ensure long-term affordability and prevent financial strain.

How long do you plan to stay?

Homeownership often makes the most financial sense for those planning to stay in one place for several years. Over time, homeowners can build equity and benefit from property appreciation. Those anticipating a short-term move may want to carefully consider whether buying aligns with their goals.

Learn More

To learn more about home financing options or to discuss your homebuying goals, click here and contact our loan department today.

Scams & Your Small Business – May ‘26

When scammers go after your business or non-profit organization, it can hurt your reputation and your bottom line. Your best protection? Learn the signs of scams that target businesses. Then tell your employees and colleagues what to look for so they can avoid scams.

Scammers’ Tactics

- Scammers pretend to be someone you trust. They impersonate a company or government agency you know to get you to pay. But it’s a scam.

- Scammers create a sense of urgency, intimidation, and fear. They want you to act before you have a chance to check out their claims. Don’t let anyone rush you to pay or to give sensitive business information.

- Scammers ask you to pay in specific ways. They often demand payment through wire transfers, cryptocurrency, or gift cards. Don’t pay anyone who demands payment this way. It’s a scam.

Protect Your Business: Train Your Employees

- Your best defense is an informed staff. Train employees not to send passwords or sensitive information by email, even if the email seems to come from a manager. Explain to your staff how scams happen and encourage them to talk with their coworkers if they suspect a scam. Order free copies of this brochure at ftc.gov/bulkorder and share them with your staff.

Verify Invoices and Payments

- Make sure procedures are clear for approving purchases and invoices and ask your staff to check all invoices closely. Pay attention to how someone asks you to pay and tell your staff to do the same. If someone demands that you pay with a wire transfer, cryptocurrency, or gift cards, don’t pay. It’s a scam.

Spot Tech-Related Scams

- Since scammers often fake their phone numbers, don’t trust caller ID. If you get an unexpected text message or email, don’t click any links, open attachments, or download files. That’s how scammers load malware onto your network or try to convince you to send money or share sensitive information. Scammers sometimes even hack into the social media accounts of people you know, sending messages that seem real — but aren’t. Learn more about protecting your small business or non-profit organization from cyber scammers and hackers: check out Cybersecurity for Small Business.

Know Who You’re Dealing With

- Before doing business with a new company, search the company’s name online with the term “scam” or “complaint.” Read what others are saying about that company. Ask people you trust for recommendations.

Learn More

For more information, visit: https://www.ftc.gov/business-guidance/resources/scams-your-small-business-guide-business

This article is a summary of the following: (DAD, M. C., & Nguyen, S. T. (2026, April 17). Protecting small businesses. Federal Trade Commission. https://www.ftc.gov/business-guidance/small-businesses

Financial Guidance for Recent Graduates – May ‘26

As college students are near graduation and preparing to transition into the workforce, Washington State Bank and the Independent Community Bankers of America® (ICBA) are providing tips to help put them on the road to a prosperous financial future.

We are here to offer tips to help graduates prepare for major financial lifecycle events:

- Start a budget. Use tools to track your income, expenses, and savings. Establishing a budget early helps build strong financial habits and prevents overspending.

- Prioritize Debt Management: Consider making extra payments on student loans or refinancing options to lower interest rates. If you have federal student loans, explore income-driven repayment options that adjust your monthly payments based on your income.

- Build a Credit History: Start with a low-limit or secured credit card to build credit. This is critical for future major purchases and may even impact your ability to secure job opportunities.

- Invest in Yourself: Explore opportunities to support professional development. Many employers offer education benefits or tuition reimbursement programs that can offset costs and lead to long-term career growth.

- Automate Savings: Setting up automatic transfers at Washington State Bank to a savings account. Even small, regular contributions can grow into significant savings over time and provide a cushion against unexpected life events.

- Understand Taxes: For many new graduates, taxes can be confusing. Ask about financial tools or resources available to ensure you're filing correctly and maximizing refunds.

“Building sound financial habits early can make a meaningful difference over time,” said ICBA President and CEO Rebeca Romero Rainey. “By working with a local community banker, individuals can develop and maintain good financial habits, creating a framework to help them develop an action plan and put their finances to work.”

To learn more about how to take control of your financial future, send us a message on our Contact Us page or stop into your nearest WSB location today.

About ICBA

The Independent Community Bankers of America® has one mission: to create and promote an environment where community banks flourish. We power the potential of the nation’s community banks through effective advocacy, education, and innovation.

As local and trusted sources of credit, America’s community banks leverage their relationship-based business model and innovative offerings to channel deposits into the neighborhoods they serve, creating jobs, fostering economic prosperity, and fueling their customers’ financial goals and dreams. For more information, visit ICBA’s website at icba.org.

How Your Deposits Help Grow Iowa Communities - Apr. '26

In this month’s Banknote Blog, we’re also highlighting how local deposits strengthen Iowa communities and support economic growth through the community banking system as April is Community Banking Month. Collectively, community banks fund nearly 60% of small-business loans and more than 80% of bank agriculture loans nationwide while contributing to local tax bases that support schools, infrastructure, and essential services.

Every time a customer deposits money into a local bank account, those dollars help businesses, farmers, and families thrive. The concept is known as fractional-reserve banking. It creates a multiplier effect: while funds generally remain fully protected and accessible to the accountholder, a portion is used by the bank to make loans within the community.

Let’s say $1,000 is deposited at WSB. The Bank holds a portion in reserves while the remaining funds may be loaned to a local farmer. When those dollars are then deposited elsewhere in the community, the process continues – supporting additional loans to small businesses, homeowners, and farmers. Through this multiplier effect, every dollar deposited in Iowa banks helps build wealth locally and expand access to credit.

Public and private deposits placed in Iowa banks remain safe and secure while continuing to serve as a foundation for responsible local lending. The dollars in your bank account truly make an impact – fueling opportunities for small businesses, supporting hardworking farmers, and creating brighter futures for families across our service area. To learn more about the value of a checking account or savings account click the buttons below, or visit your nearest Washington State Bank branch.

Savings Strategies in Honor of America Saves Week - Apr. '26

During America Saves Week (April 6-10), Washington State Bank and the Independent Community Bankers of America (ICBA) are encouraging consumers to take proactive steps to strengthen their financial resilience. Establishing a financial safety net is essential in navigating economic uncertainties and achieving long-term financial goals.

According to the Federal Reserve’s May 2025 Report on the Economic Well-Being of U.S. Households, nearly 40 percent of Americans would struggle to cover an unexpected $400 expense without resorting to borrowing or selling assets. Additionally, the U.S. personal savings rate remains well below pre-pandemic levels, standing at just 4.7 percent in Q3 2025, compared to 15 percent in 2020, according to the Federal Reserve Bank of St. Louis.

Washington State Bank and ICBA offer the following savings tips for consumers:

- Pay yourself first. Many employers offer automatic payroll deduction, which is a great way to save. Use those funds to build a retirement fund.

- Track and Prioritize Spending – Create a budget to understand where your money goes and identify areas to cut back.

- Start Small, Think Big – Saving just $5 a day (about the cost of a specialty coffee) can add up to $1,825 per year—a great foundation for an emergency fund.

- Build an Emergency Fund – Aim for at least three to six months’ worth of expenses to safeguard against financial setbacks.

- Put your tax refund to work. Nearly 84 percent of Americans plan to use their anticipated return for savings or paying off debt, rather than discretionary spending.

Where should you save?

Consider these key factors:

- Access. How quickly can you retrieve funds? Community banks use the latest technology to allow consumers the freedom to access their money when and where they need it.

- Safety. Is your money protected? The FDIC insures deposits up to $250,000 per depositor and $250,000 for certain retirement accounts. No one has ever lost a penny of FDIC-insured funds.

To learn more about the importance of saving or to open a savings account during America Saves Week, stop by your nearest WSB branch or click here to open an account today.

About ICBA

The Independent Community Bankers of America® has one mission: to create and promote an environment where community banks flourish. We power the potential of the nation’s community banks through effective advocacy, education, and innovation.

As local and trusted sources of credit, America’s community banks leverage their relationship-based business model and innovative offerings to channel deposits into the neighborhoods they serve, creating jobs, fostering economic prosperity, and fueling their customers’ financial goals and dreams. For more information, visit ICBA’s website at icba.org.

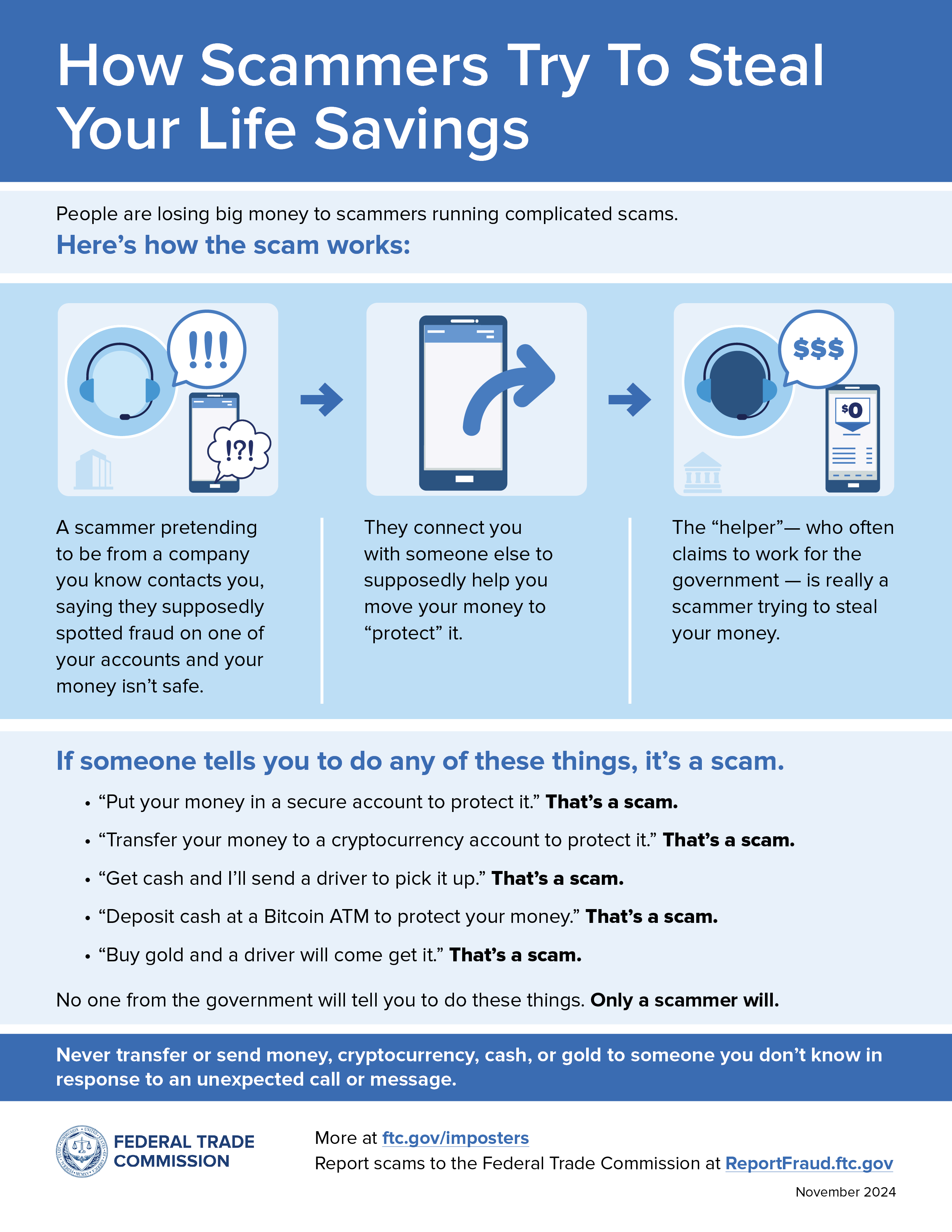

The Ins-and-Outs of Government Imposter Scams - March '26

Criminals are impersonating government agencies, law enforcement officials and regulators. Between January and September 2025, Americans filed 332,796 reports with the Federal Trade Commission, totaling $739M in losses.

HOW THE SCAM WORKS

- Unexpected contact: You get a call, text, email or message on social media claiming to be from a government or law enforcement agency, such as the FBI, Secret Service, local police or the courts.

- A manipulative story: They say your financial account was “compromised,” your identity was stolen, you’re under investigation or about to be arrested — often claiming they’re investigating fraud or trying to recover stolen money.

- The steal: They pressure you to act fast. They might tell you to withdraw cash or buy gold to hand to a courier for “safekeeping.” They might also ask you to wire money, buy cryptocurrency or share personal information like your date of birth or Social Security number. If you comply, your money — or your identity — will be stolen.

SPOT THE SCAM

Government agencies, law enforcement and regulators will never:

- Call, email, text or direct message you to demand immediate payment or threaten arrest.

- Pressure you to move or wire your money, transfer investments, or buy or invest in gold, other precious metals or cryptocurrency.

- Require payments via gift cards, peer-to-peer payment apps (e.g., CashApp, Venmo, Zelle) or crypto ATMs.

- Send couriers to collect cash, gold or valuables.

PROTECT YOURSELF

- Don’t trust caller ID. Scammers can spoof phone numbers. If they leave you a callback number, don’t use it.

- Don’t click links in unexpected messages or emails. Delete them.

- Verify before you act. Only use contact information from official sources, such as government websites or the back of your bank card.

IF YOU SUSPECT A SCAM

- End all communication, block the contact and don’t send money.

- Document everything including names, dates, contact details, websites, communications, etc.

- Report it to your financial institution, the FBI at IC3.gov or 1-800-225-5324, and local law enforcement ASAP. If it involves U.S. mail, contact the postal inspectors at 1-877-876-2455 or www.uspis.gov/report.

- Check your credit and consider placing security freezes or fraud alerts with Equifax, Experian and TransUnion.

- Get professional help from a financial counselor, attorney and/or licensed tax specialist.

Tips to Boost Financial Confidence During Credit Education Month – Mar. ‘26

In recognition of Credit Education Month Washington State Bank and the Independent Community Bankers of America® (ICBA) are encouraging consumers to strengthen their financial well-being by building healthy credit habits and establishing long-term savings strategies.

To support consumers during Credit Education Month, WSB and the ICBA encourage individuals to consider the following steps:

- Pay yourself first. Automate savings contributions to build consistency and momentum. Set these up easily within your WSB Online Banking or Mobile Banking app under the ‘Transfer’ tab.

- Track spending and plan ahead. Create a budget to find opportunities to save and avoid debt.

- Build an emergency fund. Aim to set aside three to six months to cover essential expenses. Opening a specific savings account for your emergency fund can help keep things organized and still readily available. Set up an automatic transfer to the account and watch it grow each month!

- Use credit responsibly. Make payments on time, keep balances manageable, and avoid opening or closing accounts unnecessarily.

- Monitor credit regularly. Review credit reports to spot errors, detect fraud early, and understand how financial behaviors impact credit standing. Take advantage of the My Financial Health widget inside your WSB Online Banking and Mobile Banking app. Here you can find your credit score, monitor subscriptions, and screen your identity online.

“Strong credit and smart saving go hand in hand,” ICBA President and CEO Rebeca Romero Rainey said. “Understanding how to manage credit, build savings, and plan ahead is essential to long-term financial security. “Community banks are uniquely positioned to provide personalized guidance and trusted financial solutions that help individuals build resilience, plan for the future, and achieve lasting financial success.”

To learn more about improving your financial health or to speak with a local banker, stop by a nearby branch during Credit Education Month.

About ICBA

The Independent Community Bankers of America® has one mission: to create and promote an environment where community banks flourish. We power the potential of the nation’s community banks through effective advocacy, education, and innovation.

As local and trusted sources of credit, America’s community banks leverage their relationship-based business model and innovative offerings to channel deposits into the neighborhoods they serve, creating jobs, fostering economic prosperity, and fueling their customers’ financial goals and dreams. For more information, visit ICBA’s website at icba.org.

Top Five Fraud Trends to Be Aware Of – Feb. ‘26

National Safer Internet Day is Feb. 10, and WSB is encouraging customers to strengthen online habits and stay alert to the rising number of digital scams. Fraud activity continues to climb nationwide. According to the Federal Trade Commission (FTC), consumers reported more than $12.5 billion in losses in 2024 – a 25% increase from the prior year.

Investment scams had the highest monetary loss in 2024 with $5.7 billion in losses, followed by $2.9 billion lost to imposter scams. Consumers also lost more money through bank transfers and cryptocurrency than all other payment methods combined. These trends continue to rise, with scammers adopting more aggressive tactics, including artificial intelligence (AI)-generated impersonation, social media-based deception and more.

Here are the top five fraud categories reported in 2025, based on Federal Trade Commission data.

- Imposter scams – 516,724 reports

Imposter scams remain the most reported fraud type in the country. Scammers continue posing as banks, government agencies, family members or well-known companies; now using AI-generated voices, spoofed phone numbers or convincing emails. These scams pressure people to act quickly, send money or share account information. Customers should verify any unexpected request by contacting the organization or person directly using a verified phone number.

- Online shopping and negative reviews – 193,020 reports

Online shopping scams continue to grow, driven by fraudulent ads on Facebook, Instagram, TikTok and other platforms. In August 2025, the FTC warned consumers about “big discount” social media ads impersonating real brands, which often link to fake websites designed to steal money or personal information. Shoppers may receive a counterfeit product or nothing at all.

To stay safe, research the seller, compare prices and use a credit card for purchases. Scammers often push customers toward gift cards, wire transfers, payment apps, or cryptocurrency – all red flags.

- Internet services – 118,071 reports

These scams include fake tech-support calls, phony antivirus subscriptions, and pop-up warnings claiming your device is compromised. Scammers often request remote access or immediate payment. Avoid clicking on pop-ups and contact service providers using verified customer service numbers.

- Business and job opportunities – 75,364 reports

Scammers continue targeting people searching for jobs or supplemental income. Fake job postings, business “starter kits,” and work-from-home offers often require upfront payment or ask applicants to transfer money during the “hiring process.” Legitimate employers never ask new hires to pay fees or move funds for them.

- Investment-related scams – 66,703 reports

Investment scams remain one of the most expensive fraud categories. High-pressure cryptocurrency schemes, fake trading platforms and AI-driven “advisors” continue to promise guaranteed returns. If an investment sounds too good to be true, it likely is. Independent verification is critical.

These tips are provided by the Iowa Bankers Association.

Common Types of Identity Theft – Jan. ‘26

In observance of Identity Theft Awareness Week, Washington State Bank encourages consumers to be aware of the many different types of identity theft and how to avoid it. The Federal Trade Commission received more than 1 million reports of identity theft in 2024, with credit card abuse being the main method of identity theft.

Washington State Bank encourages you to stay aware of common types of identity theft and how to avoid it:

Account takeover fraud – In this type of fraud, scammers use stolen information like usernames, passwords and account numbers to take over social media and bank accounts. Then, they reset passwords or emails to lock the user out of their own accounts.

- Action step – Enable multifactor authentication (MFA) and consider using a password manager. MFA adds an extra security step to prevent unauthorized access even if your password is stolen. Password managers create strong, difficult-to-guess passwords to keep criminals at bay.

Debit and credit card fraud – Fraudsters use stolen account information to withdraw funds or make purchases with your card.

- Action step – Put a freeze on cards the minute they’ve been lost or misplaced and quickly request a new card if the card does not turn up soon. Additionally, regularly monitor accounts for suspicious transactions and report them immediately.

Tax fraud – With tax season in full swing, it’s important to avoid fraudsters posing as the IRS. This occurs when criminals use your Social Security number to file a tax return to steal your refund.

- Action step – Be aware the IRS will always make its first official contact via mail. Do not answer or respond to any supposed calls or texts from the IRS if you haven’t first received a letter.

Learn More

For more information on common identity theft tactics, visit the Federal Trade Commissions website: https://consumer.ftc.gov/identity-theft-and-online-security/identity-theft.

These tips are provided by the Iowa Bankers Association.

Recap Your Financial Year and Plan for the Next- Dec. ‘25

With the end of 2025 drawing near, it’s a great time to look back at spending patterns and habits, review savings and investments, make a plan for paying off debt, and set financial goals for the upcoming year. By taking a few simple steps at the end of the year, you can enter 2026 feeling organized and confident about meeting your financial goals. Washington State Bank has steps you can take to achieve your financial goals.

Review accounts — Before setting new goals, take the time to closely review financial information like bank and investment accounts, credit card bills, loan balances and any outstanding debt. Be sure your spending aligns with your goals.

Analyze spending habits — Identify areas where you spent more than you planned to, like non-essentials, eating out or unused subscriptions. Whatever it is, make a budget for it and stay within that budget — small adjustments can make a major impact in the new year.

Evaluate savings and investments — Assess whether you’re staying on track with savings and investment goals. Increase contributions to IRAs or 401(k) accounts if possible and consider rebalancing your investment portfolio.

Get ready for tax season — Stay organized by gathering documents like paystubs, donation and deductible expense receipts ahead of tax season.

Establish goals for the upcoming year — After taking the time to reflect and assess, use these insights to set realistic and timely goals. Consider using a budget-tracking app or mastering an Excel spreadsheet. Decide what milestones you’re striving toward — retirement, buying a house, or saving for college.Don’t Let Scammers Steal Your Joy This Season – Nov. ‘25

International Fraud Awareness Week is coming up (November 16th-22nd), and Washington State Bank is urging consumers to use extra caution online this holiday season. Scammers take advantage of unique opportunities during the holiday season to defraud consumers. These involve phishing emails, charity scams, delivery scams and travel scams. The busyness of the season makes scams easier to miss, and in 2024, nearly 60% of the U.S. population made a purchase during Cyber Week (Thanksgiving through Cyber Monday).

During the season of giving, make sure scammers don’t steal your sensitive information and money by learning about these common types of scams during the holiday season:

- Phishing scams – Online shopping makes it easy to complete the gifting checklist, but also presents more opportunities for fake deals, counterfeit websites, and prices that are a “little too-good-to-be-true.” Be wary of clicking on links from social media ads or buying from websites without “https” in the URL.

- Charity scams – Fraudsters want to capitalize on people’s generosity during the holiday season by creating fake charities and organizations. Counterfeit charities may play on people’s emotions, pressure them to donate, ask for forms of payment like crypto or gift cards, and are vague about where exactly the money is going. Research the legitimacy of charities on websites like BBB Wise Giving Alliance and Charity Navigator before donating.

- Delivery scams – Online shopping means the anticipation of package deliveries and receiving delivery status updates. Scammers may send phony emails with fake delivery updates, pretending to be FedEx, Amazon, and UPS and attempt to get you to share personal information. Keep in mind – these companies won’t send unsolicited messages asking for personal or payment information.

- Travel scams – Fake travel agencies may advertise discounts on airfare, luring people who travel during the holiday season. These scams are especially malicious because of sensitive information needed for legitimate travel like your address and credit or debit information. Double check URLs and be wary if your login information isn’t working on travel websites.

Tips in Honor of World Financial Planning Day – Oct. ‘25

Financial planning is something every age group can participate in, and in honor of World Financial Planning Day on October 8th, Washington State Bank is encouraging people of all ages to set aside time to evaluate financial goals.

According to Motley Fool Money, the average American scores just 48% on financial literacy tests. From childhood to retirement, financial planning and literacy is about more than just numbers — it’s about achieving milestones, aligning money with your goals, and providing peace of mind. Take steps to improve financial literacy and planning. There are unique focuses for each age group when it comes to financial planning. Here’s a few recommendations for every phase of life.

Teens and younger – It’s important to teach financial literacy to younger people. Start with a simple budget, like the 50/30/20 rule for needs, wants and savings. Instilling confidence at a young age sets kids up to handle bigger responsibilities down the road.

In your 20s – You can build a lifetime’s worth of wealth by building a strong foundation in your 20s. Start investing for retirement, start an emergency fund, and work to establish healthy habits by distinguishing between needs and wants. It’s also a great time to chip away at high-interest debt from higher education, credit card, or car loans.

In your 30s and 40s – Strive to increase retirement contributions as income levels grow. Continue to save for major goals, like buying a house, growing your family, or paying for a child’s education.

In your 50s and 60s – As retirement nears, shift priorities toward protecting wealth and preparing for life post-workforce. Plan withdrawal strategies, pay off any remaining debt, and continue strong investment strategy.

These tips are provided by the Iowa Bankers Association.

7 Strategies for Spotting Counterfeit Money

The process of producing counterfeit currency continues to grow more sophisticated, especially with recent advancements in technology. But there are still plenty of telltale signs that can help you and your employees distinguish counterfeit money vs. real money. Do you know how to detect counterfeit bills? Here’s what to look for when you receive cash from customers.

- Check the Feel of the Paper

The texture of real currency is distinct because of the special paper it is printed on. When you’re holding an authentic banknote, feel the bill and note the difference in texture compared to fake money.

- Examine Borders and Printing

Another tip is to inspect the borders and edges of bills. Counterfeit money often has uneven or blurry printing. A counterfeit U.S. bill may even appear crooked. On the other hand, legitimate currency will have crisp, well-defined edges.

Theatrical currency can appear to be legitimate to the naked eye. Look closely for verbiage like, “For Motion Picture Purposes” or “COPY” printed along the bill as well as misspelled words.

- Look For Red and Blue Threads

Real U.S. bills have embedded red and blue threads in the paper. You’ll know a bill’s fake when it has printed or missing threads instead. Thus, looking for the proper-colored threads is a quick authenticity check to distinguish fake money vs. real money.

- Inspect Serial Numbers

When learning how to check for counterfeit money, you should also pay attention to the serial numbers shown on bills. The serial numbers on a single bill should be the same. So, if you notice a bill has mismatched serial numbers, it’s another good indication that it’s counterfeit.

- Check For Security Threads

When you’re learning how to spot fake money, looking for the security thread – and ensuring it’s in the proper location – is highly important. You should only see it when you hold the bill up to the light. If it’s on the wrong side of the face for the denomination, it’s likely fake. Since 2009, $100 bills have featured a blue security ribbon woven into the paper — not printed on it. Make sure to look for this feature when accepting a $100 bill, tilting the banknote to ensure the holographic images shift in the blue ribbon.

- Look For Ink Bleeding or Smudging

Inspect all bills for ink inconsistencies that may indicate it’s fake, such as bleeding or smudging. These are signs of poor printing quality, as real currency does not have ink that will react in this manner.

How to Protect Your Business from Counterfeit Money

Cash handling procedures for restaurants, retailers, and other types of cash-heavy businesses should consider including the above authenticity checks. Taking proactive steps like proper staff training can help safeguard your business from counterfeit bills.

Click here for a visual of signs to look for.

These helpful hints to aid in detection of counterfeit currency do not guarantee the genuineness of any banknote.

This article is a summary of the following: https://integratedcashlogistics.com/how-to-spot-counterfeit-money/